All Categories

Featured

Table of Contents

The round figure is calculated to be today value of payments, which indicates it would certainly be less than if the recipient proceeded the continuing to be repayments. As a choice, let's claim the proprietor selected a joint income, covering the proprietor's and a partner's lives. The proprietor might pick a feature that would certainly continue payments of 100% to the surviving partner or pick a various percent, such as 50% or 75% of the initial repayment.

As an exception to the five-year guideline, the IRS likewise enables you to stretch the repayments out over a period not surpassing your life span. This option may not be available in all agreements, nevertheless, and it isn't offered when the beneficiary isn't a living individual, such as a trust or charity.

Spouses and certain various other beneficiaries have added alternatives. If you're an enduring spousal beneficiary, you have a few alternatives for moving on. You can move the agreement into your name. If you choose this alternative, you can continue with the initial regards to the annuity agreement as though the annuity were your own.

To understand the tax consequences of inherited annuities, it's crucial to initially recognize the distinction in between professional and nonqualified annuities. The difference between these two kinds of annuities isn't due to agreement terms or framework however how they're purchased: Qualified annuities are purchased with pretax dollars inside of retirement accounts like.

Payments from nonqualified annuities are just partially taxable. Because the cash utilized to buy the annuity has actually currently been taxed, only the section of the payout that's attributable to incomes will be consisted of in your earnings. How you pick to get the fatality advantage is also a factor in figuring out the tax obligation ramifications of an acquired annuity: Taxes of lump-sum payouts.

Annuity Death Benefits inheritance and taxes explained

Tax of settlement streams. When the death advantage is paid out as a stream of payments, the tax obligation liability is spread out over several tax years.

For a certified annuity, the entire payment will be reported as taxed. If you acquire an annuity, it's essential to consider taxes.

Tax consequences of inheriting a Annuity Income Stream

Inheriting an annuity can offer an exceptional chance for you to make development toward your goals. Prior to you decide what to do with your inheritance, think of your goals and exactly how this cash can assist you attain them. If you currently have a monetary plan in area, you can begin by assessing it and thinking about which objectives you might want to obtain ahead on.

Everybody's scenarios are different, and you need a strategy that's personalized for you. Link with a to discuss your inquiries regarding inheritances and annuities.

Learn why annuities require beneficiaries and how inherited annuities are handed down to beneficiaries in this article from Safety - Deferred annuities. Annuities are a method to guarantee a routine payout in retirement, yet what occurs if you pass away before or while you are receiving settlements from your annuity? This write-up will clarify the basics of annuity death benefits, including who can get them and just how

If you die before launching those payments, your enjoyed ones can collect money from the annuity in the kind of a survivor benefit. This makes sure that the recipients take advantage of the funds that you have actually conserved or bought the annuity contract. Beneficiaries are very important since they collect the payout from your annuity after you pass away.

It is necessary to maintain your checklist of beneficiaries upgraded. As an example, a separation could trigger an upgrade to your assigned beneficiary. Does a recipient on an annuity supersede a will - Annuity withdrawal options.?.!? The annuity death advantage applies to beneficiaries independently of the will. This indicates the annuity benefit goes to one of the most lately designated primary beneficiary (or the additional, if the primary recipient has actually died or is unable of accumulating).

Taxation of inherited Annuity Income

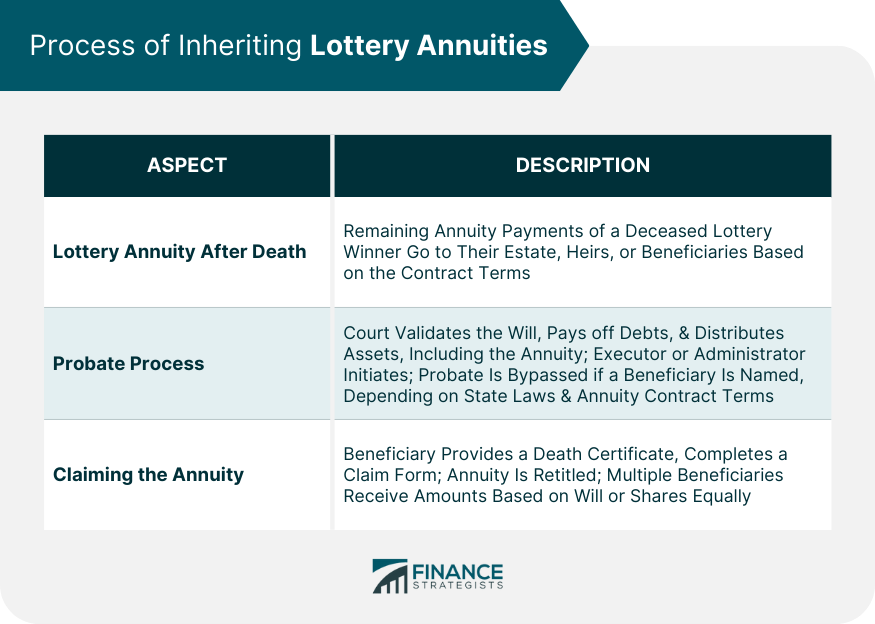

That makes it more complex to obtain the annuity funds to the intended individual after you pass. In many states, an annuity without a recipient ends up being part of your estate and will be paid according to your will. That includes a probate procedure, in which a dead individual's home is examined and their will verified prior to paying any outstanding tax obligations or financial debts and after that dispersing to recipients.

It is exceptionally challenging to test a standing contract, and bench for showing such an instance is incredibly high. What occurs to an annuity upon the fatality of an owner/annuitant depends upon the kind of annuity and whether or not annuity settlements had started at the time of death.

If annuity settlements have begun, whether or not repayments will continue to a called recipient would certainly depend on the kind of annuity payout selected. A straight-life annuity payout will spend for the life of the annuitant with repayments stopping upon their death. A period-certain annuity pays for a certain time period, suggesting that if the annuitant dies throughout that time, settlements would certainly pass to a recipient for the rest of the specific period.

{kind=link}

Table of Contents

Latest Posts

Understanding Financial Strategies A Closer Look at How Retirement Planning Works What Is Immediate Fixed Annuity Vs Variable Annuity? Pros and Cons of Fixed Vs Variable Annuity Pros Cons Why Fixed In

Decoding How Investment Plans Work Everything You Need to Know About Financial Strategies What Is Fixed Vs Variable Annuity Pros And Cons? Advantages and Disadvantages of Different Retirement Plans Wh

Analyzing Variable Annuity Vs Fixed Annuity Everything You Need to Know About Financial Strategies What Is the Best Retirement Option? Pros and Cons of Various Financial Options Why Fixed Annuity Or V

More

Latest Posts